Mortgage Refinance Rates: Your Guide to Lower Monthly Payments and Financial Freedom

Mortgage Refinance Rates: Your Guide to Lower Monthly Payments and Financial Freedom

Are you feeling the pinch of high mortgage payments? Are you curious about whether refinancing your mortgage could provide some much-needed financial relief? You’re not alone. Millions of homeowners explore mortgage refinancing each year, seeking better rates, lower monthly payments, or access to equity. Understanding mortgage refinance rates is the first step towards making an informed decision that can significantly impact your financial future. This comprehensive guide will delve into everything you need to know about current refinance rates, the process, and how to determine if refinancing is right for you.

Understanding Mortgage Refinance Rates

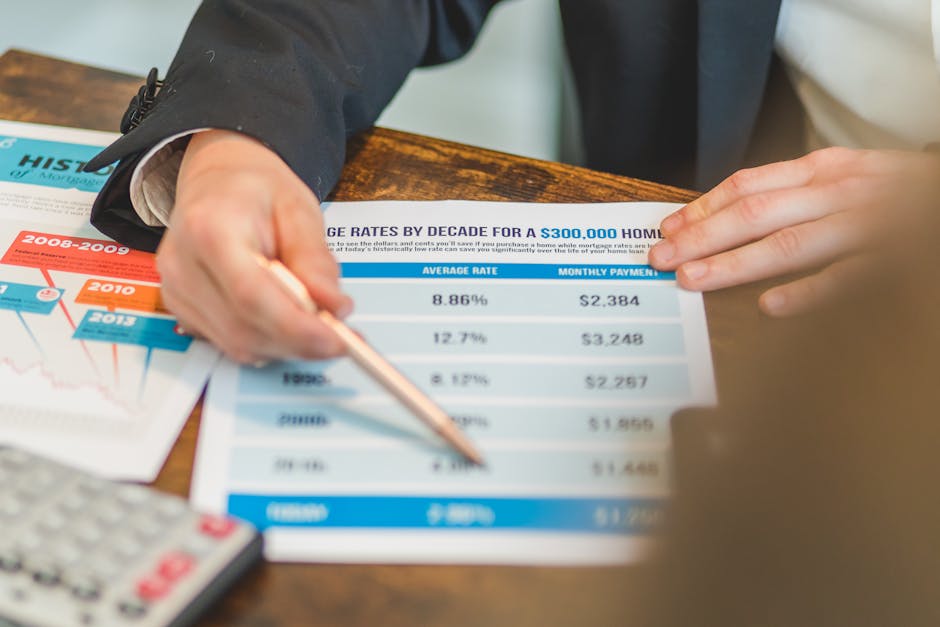

Mortgage refinance rates are the interest rates lenders charge for replacing your existing mortgage with a new one. These rates fluctuate constantly, influenced by various economic factors like the Federal Reserve’s monetary policy, inflation, and overall market conditions. Unlike fixed-rate mortgages, refinance rates are dynamic and are often presented as an Annual Percentage Rate (APR), reflecting the total cost of borrowing including fees and interest.

Factors Affecting Refinance Rates

- Credit Score: Your credit score is a crucial determinant of the rate you’ll qualify for. A higher credit score typically translates to a lower interest rate.

- Loan-to-Value Ratio (LTV): This ratio compares the amount you owe on your mortgage to the current value of your home. A lower LTV generally leads to better rates.

- Debt-to-Income Ratio (DTI): This compares your total monthly debt payments to your gross monthly income. A lower DTI indicates greater affordability and can improve your chances of securing a favorable rate.

- Interest Rate Environment: Prevailing interest rates set by the Federal Reserve significantly influence mortgage refinance rates. Lower rates make refinancing more attractive.

- Loan Type: Different loan types, such as conventional, FHA, VA, or USDA loans, come with varying rate structures and eligibility criteria.

- Mortgage Term: The length of your new mortgage (e.g., 15 years, 30 years) will also affect the rate. Shorter terms usually mean higher monthly payments but lower overall interest paid.

How to Find the Best Mortgage Refinance Rates

Finding the best refinance rate requires diligent research and comparison shopping. Don’t settle for the first offer you receive. Here’s a systematic approach:

- Check Current Market Rates: Several online resources provide up-to-date information on mortgage refinance rates. These websites often allow you to input your financial information to receive personalized rate estimates.

- Shop Around: Contact multiple lenders, including banks, credit unions, and mortgage brokers. Compare their rates, fees, and terms before making a decision.

- Consider Your Financial Goals: Define your objectives for refinancing. Are you looking to lower your monthly payment, shorten your loan term, or access equity? This will help you choose the right type of refinance.

- Review the Fine Print: Carefully examine the loan documents, paying close attention to any associated fees, prepayment penalties, and other terms and conditions.

- Get Pre-Approved: Before committing to a refinance, obtain pre-approval from several lenders. This will give you a clearer picture of your eligibility and potential rates.

Types of Mortgage Refinances

Several refinance options cater to different financial situations:

Rate-and-Term Refinance

This refinance allows you to lower your interest rate, shorten your loan term, or both. It’s ideal for borrowers seeking lower monthly payments or faster loan payoff.

Cash-Out Refinance

This option lets you borrow more money than your current mortgage balance, giving you access to your home’s equity. The extra cash can be used for home improvements, debt consolidation, or other expenses. However, be mindful of increased debt and potential risks.

No-Cash-Out Refinance

This refinance allows you to simply switch to a lower interest rate without borrowing additional funds. It’s a cost-effective way to reduce your monthly payments.

Is Refinancing Right for You?

Refinancing isn’t always the best option. Carefully weigh the pros and cons:

Pros:

- Lower monthly payments

- Reduced overall interest paid

- Access to home equity

- Consolidation of debt

- Improved financial flexibility

Cons:

- Closing costs

- Potential for increased total interest paid if you extend the loan term

- Time-consuming process

- Credit score impact during application

- Potential for unforeseen issues during appraisal or underwriting

Use a refinance calculator to estimate potential savings and determine if the benefits outweigh the costs. Consider factors such as your current interest rate, remaining loan term, and the potential reduction in monthly payments.

Choosing the Right Lender

Selecting a reputable lender is crucial for a smooth and successful refinance process. Look for lenders with:

- Competitive rates and fees

- Positive customer reviews and ratings

- Transparent and clear communication

- Experienced and knowledgeable loan officers

- A streamlined and efficient process

Navigating the Refinance Process

The refinance process typically involves these steps:

- Pre-qualification: Get pre-qualified to understand your borrowing power and potential rates.

- Application: Submit a complete loan application, including financial documents.

- Loan Approval: The lender reviews your application and approves the loan.

- Appraisal: An appraiser assesses your home’s value to ensure it meets the lender’s requirements.

- Closing: You sign the loan documents and officially finalize the refinance.

Staying Informed about Mortgage Refinance Rates

Mortgage refinance rates are dynamic. Staying informed is key. Regularly monitor market trends, track changes in interest rates, and consult financial professionals to make timely and effective refinancing decisions. Understanding mortgage refinance rates isn’t just about finding a lower monthly payment; it’s about making sound financial choices that can positively shape your future.